Real estate still attractive despite short-term turbulence

By Bruce Wan,

head of Asia Real Assets Research,

B;lackRock

/ EdgeProp Singapore |

SINGAPORE (EDGEPROP) - The early part of 2020 is proving to be a little more eventful than usual, as the outbreak of the Covid-19 coronavirus drives widespread disruption to economic activity and investor confidence. Already, there is obvious economic impact across Asia, with temporary factory, office and school closures.

Increasingly, despite more stringent travel restrictions, the impact has broadened to other parts of the world through secondary outbreaks. Policymakers are responding to this with aggressive containment measures and sizeable monetary and fiscal stimulus.

Increasingly, despite more stringent travel restrictions, the impact of Covid-19 has broadened to other parts of the world through secondary outbreaks.(Photo: Bloomberg)

From a real estate market perspective, the impact is likely to be the most acute in the hospitality and retail sectors in Hong Kong and mainland China, where we expect more signs of value to emerge in 2020, particularly for nimble investors with ready capital. Meanwhile, homebound, telecommuting and tele-schooling households will progressively add to long-term demand for last-mile logistics and digital infrastructure.

Once there are more tangible signs of viral containment and market stabilisation, pricing dynamics will revert to longer-term drivers, reflecting structural demand growth, lower interest rates, the continuing shift to yield assets, abundant capital for deployment and early signs of diminishing trade tensions, notwithstanding a near-term dip in economic activity and elevated geopolitical tensions.

Long-term cycle intact

Near-term disruptions aside, the long-running structural themes for 2020 and beyond can be summarised as follows: real asset markets are gradually going through the market cycle, still relatively attractive and relentlessly changing with the times.

The long-term cycle is still intact, though there are some near-term disruptions. Low interest rates and abundant capital are still supportive of the investment outlook. Market cycles are quite divergent, with resilient US market conditions, some moderation in Europe and a slowing in China given slower trade and the virus outbreak. For investors, this variability within a long-term cycle provides considerable scope for active market selection and diversification gains across a globalised portfolio.

The property sector remains relatively attractive, with risk-adjusted returns that compare well to other asset classes, especially in a world with moderating returns expectations. Indeed, the scope for consistent yield is compelling given low-yielding bonds. This is prompting a continuing portfolio reallocation to both infrastructure and real estate. Moreover, lower interest rates are still supporting tight cap rates, although investors should prudently target segments with firm income growth prospects, either from contracted revenue gains or well-occupied, under-supplied real estate markets.

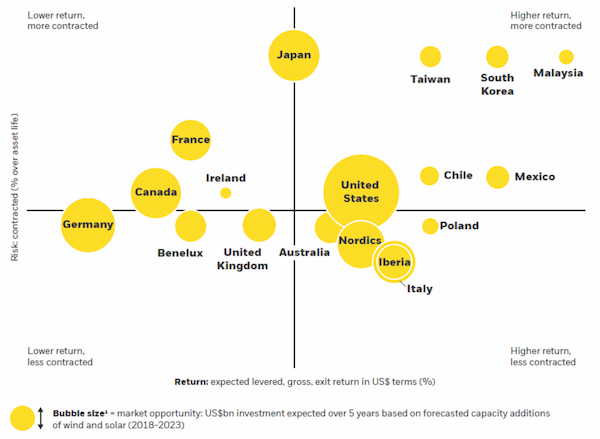

Global Renewable Pricing Environment

Capacity market data is taken from Bloomberg New Energy Finance.

Source: BLACKROCK, PROPRIETARY ANALYSIS PERFORMED BY THE GLOBAL RENEWABLE POWER TEAM, AS OF OCTOBER 2019

Structural changes

Relentless structural changes continue to be crucial drivers of long-term demand and profitability. In real assets, our investment horizon is somewhat longer by necessity. Consequently, we focus keenly on the impact of demographic change, supply-side growth, technological change and, increasingly, climate risk. In the last area, we are focused on driving change in investing for climate sustainability via changes to investment strategies, improved disclosures, and a sharper focus on potential environmental, social and governance (ESG) risks.

In this context, the market drivers are both global and local, and investors need to tailor their strategies accordingly.

For infrastructure, energy transition – from carbon-intensive to renewable sources – remains the dominant theme driving asset allocation and deal flows. In Asia, underlying energy demand remains robust, with investment opportunities broadening outside of core markets like Australia and Japan as regulatory frameworks improve. In the US, there is a prominent remaking of the energy sector in progress, where a concerted push into LNG (liquefied natural gas) will underpin transport and processing infrastructure, while the renewables and power storage segments are maturing rapidly. In Europe, the push into renewables continues at a robust pace, enabled by a more supportive political framework and EU emission targets.

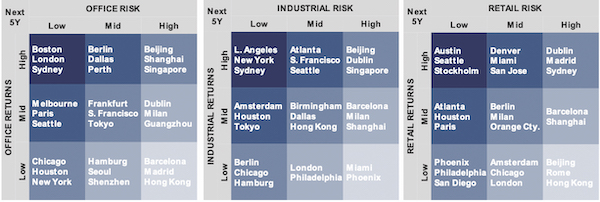

Target Market Analysis (February 2020)

Source: BLACKROCK REAL ASSETS

Abundant yield-seeking capital

For real estate, abundant yield-seeking capital continues to support deal volumes, even as tighter pricing, viral disruptions and geopolitical tensions prompt near-term caution in markets. In Asia, there is a differentiated outlook: firmer growth overall, but sharp disruptions in Hong Kong and mainland China – given trade barriers and the virus outbreak – are providing emerging value. In the US, the e-commerce shift is still changing asset allocation and driving market returns, in favour of logistics and at the expense of traditional retail. In Europe, there is slightly more clarity for investors post-Brexit, as focus turns to sectors with supportive tailwinds, including build-to-core, logistics and student accommodation.

As real estate markets are somewhat more comparable, we project the outlook using BlackRock’s Target Market Analysis framework, which sets out return and risk expectations across 50 cities and four sectors over the next five years. In this way, our 2020 outlook for internal investment teams can be expressed in actionable terms, highlighting Boston, Berlin and Sydney as key office targets; New York, Los Angeles and Sydney as priority picks for industrial; and Austin, Seattle and Stockholm as points of focus for retail.

All told, investing well is always an achievable challenge, and 2020 looks to be no different. And while it is common to focus on the news headlines – on trade, politics or viruses – the key drivers of long-term value and returns are predominantly structural. In this context, our investment course for 2020 is well set, with a clear focus on cyclical drivers, relative value and deep structural drivers of real asset demand.

Bruce Wan is BlackRock’s head of Asia Real Assets Research

Read also:

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Subscribe to our newsletter

Top Articles

Search Articles