Real estate investments up 11.5% q-o-q in 1Q2021, led by residential

By Valerie Kor

/ EdgeProp Singapore |

SINGAPORE (EDGEPROP) - Singapore’s real estate market is on the road to recovery, according to CBRE’s MarketView 1Q2021 Real Estate Market Performance report. Preliminary real estate investment volume increased by 11.5% q-o-q to $3.52 billion for 1Q2021. It is the third consecutive quarter of increase since 2Q2020 when Singapore went through the “circuit breaker” period.

The report states that residential investments outperformed the rest of the other segments, accounting for 37.8% of investment sales with the sale of private sites and strong luxury sales.

Three sites at Institution Hill were sold en bloc to a local consortium comprising Macly Group, Roxy-Pacific Holdings and construction firm LWH Holdings for $33.6 million in February. Just off River Valley Road, the sites have a total land area of 8,761 sq ft and can be developed into a new residential project with a total gross floor area of 24,530 sq ft.

Additionally, 2, 4 and 6 Mount Emily Road in District 9 were sold to ZACD International at $18 million and Surrey Point in District 11 was acquired by an Amara Holdings joint venture for $47.8 million.

The luxury segment also performed well, notes the report, pointing out that in 1Q2021, 18 good class bungalows were sold and 31 units transacted at above $10 million. Notably, 20-unit luxury development Eden by Swire Properties made headlines when it was sold collectively for $293 million.

Industrial sales came in second to residential sales, amounting to $967.46 million. It was boosted by a portfolio transaction of assets injected into the Boustead Industrial Fund by Boustead Projects.

Other sizeable capital market transactions came from the office sector, such as the sale of a 50% stake in OUE for $633.75 million and the $150 million sale of Certis Cisco Centre to a trust set up by Certis and Lendlease for redevelopment.

Recovery was also seen in the residential, office, industrial and retail sectors.

Strong demand for RCR and CCR homes

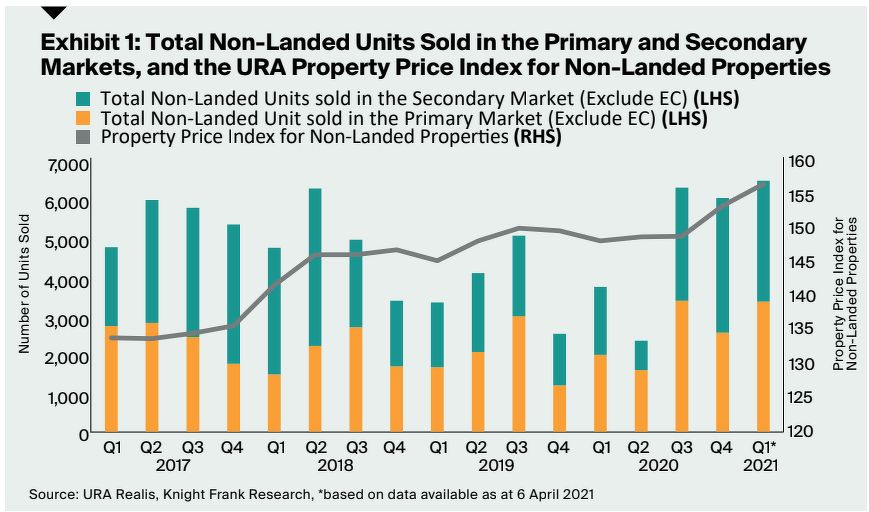

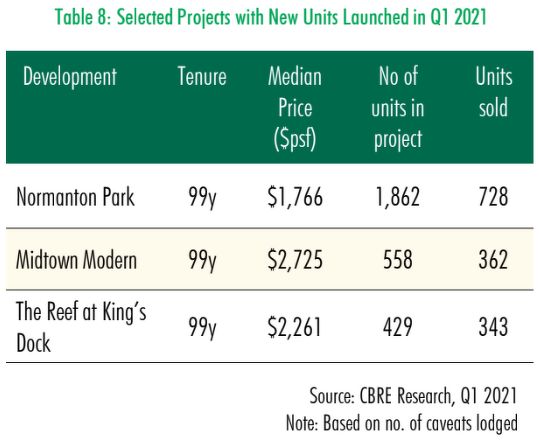

Overall, the residential market performed well, according to Knight Frank’s Residential 1Q2021 report. In 1Q2021, 3,357 non-landed new private homes were sold, which is 31.6% higher than the previous quarter. The increase came from a number of launches in the first three months of 2021: Normanton Park, Midtown Modern and The Reef at King’s Dock.

In total, 6,470 non-landed private units, excluding ECs, changed hands in 1Q2021, which was 7.3% and 73.5% higher q-o-q and y-o-y respectively. Knight Frank suggests the demand came from HDB upgraders, retiree downgraders, and the children of an older generation who is “recycling substantial property capital gains” and helping their children with their property purchases.

According to URA’s flash estimates, private residential property prices rose for the fourth consecutive quarter in 1Q2021, growing by another 2.9% q-o-q after a 2.1% increase in the previous quarter. CBRE believes that the rising prices are driven by “increasing buyers’ confidence, pent-up demand and a low-interest-rate environment”.

In the Rest of Central Region (RCR), secondary transactions declined but there was an 87.5% q-o-q increase in primary sale volumes to 1,746 units, which more than made up for the decrease. This was due to the launch of The Reef at King’s Dock, which offered 429 units, and Normanton Park, which offered 1,862 units. These two projects sold 1,070 units combined in 1Q2021.

CBRE notes that transactions at The Reef at King’s Dock, which achieved a median pricing of $2.261 psf, were likely to have contributed to the higher psf pricing in the Rest of Central Region (RCR). It also concurs with Knight Frank that there is resilient demand from upgraders.

Additionally, Knight Frank’s report also states that the number of units sold in the Core Central Region in 1Q2021 was higher than every quarter in 2020 as there was a lack of new launches last year. This segment will see a pick-up in momentum in March with the new launches of Midtown Modern and The Atelier. Midtown Modern has sold 362 units at an average of $2,774 psf in 1Q2021. The Atelier in District 9 sold four out of 120 units in March at an average price of $2,904 psf.

Knight Frank observes that in 1Q2020, buyers were drawn to penthouse units of older developments with large sizes. At least 15 penthouses above 3,000 sq ft, which were completed between 1998 and 2013, changed hands. They were sold between $5.4 million and $18 million, the most expensive one being a 7,266 sq ft penthouse in St Regis Residences Singapore.

Private property prices have increased by 6.2% since 1Q2020, which has exceeded the government’s GDP growth forecast of 4 to 6%, notes CBRE. The launch of upcoming projects at higher psf pricing might also continue to push the price index higher. CBRE expects new home sales to fall within the region of 9,000 to 10,000 for 2021.

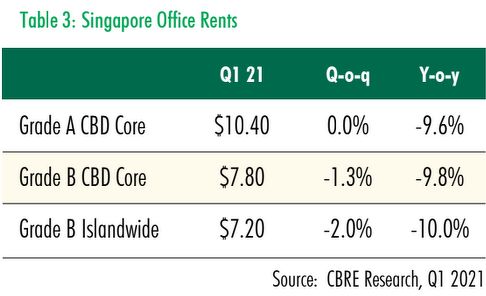

Grade A office rents held steady

After three quarters of negative net absorption, the office market registered a positive net absorption of 0.13 million sq ft in 1Q2021. This was led by Dyson, who has leased 110,000 sq ft of office space at the redeveloped St James.

CBRE observes that Grade A market also registered positive net absorption as occupiers capitalised on the declining rents and moved to prime office buildings. The demand primarily came from technology and financial services industries such as asset management firms as well as family offices.

Additionally, tenants who were displaced from older buildings in the CBD that are scheduled for redevelopment such as AXA Tower and Fuji Xerox Towers, have been on the lookout for space and contributed to increased occupier activity.

As Grade A (Core CBD) office space remained tight, rental decline slowed after four quarters. In 1Q2021, Grade A (Core CBD) rents remained stable q-o-q at $10.40 psf/month. On the flipside, Grade B office spaces continue to grapple with higher vacancy rates and saw a further rental decline of 1.3% q-o-q to $7.80 psf/month.

The recovery of the office market will not be even, concludes CBRE. However, demand will increase together with the gradual recovery of the economy.

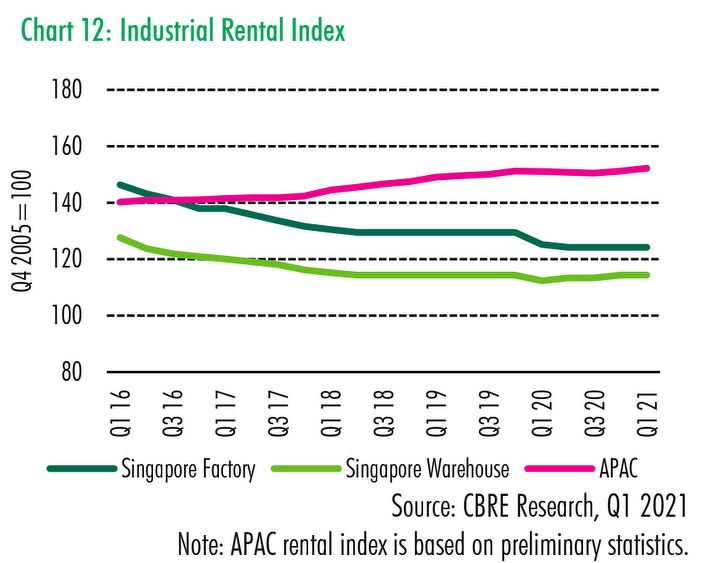

Industrial segment to remain two-tier

CBRE’s report states that Singapore’s manufacturing sector sustained steady growth, supported by electronics, biomedical manufacturing and precision engineering clusters. This resulted in stable leasing activity in 1Q2021.

Warehousing continues to be driven by third-party logistics, e-commerce and food logistics segments. High-tech factory buildings from the semiconductor, precision engineering and technology segments also saw some leasing activity.

Rents for factories and warehouses stayed resilient, holding stable q-o-q, while prime logistics rents grew 0.7% q-o-q to $1.39 psf/month in 1Q2021.

The factory submarket remains two-tier. High-specs buildings will continue to be in demand along with the recovery of the manufacturing sector while older buildings may continue to weigh on overall rental performance.

Retailers are increasing their footprint

CBRE says that retail indicators have showed signs of recovery. Compared to January, when retail sales decreased 1.3% y-o-y, retail sales increased by 3.5% y-o-y in February. CBRE observes that in 1Q2021, retailers are increasing their footprint and reinventing new concepts but their decision-making process is longer.

There has also been a slowdown in rental declines of prime retail spaces in 1Q2021, from a decrease of 3.6% q-o-q in 4Q2020 to a decrease of 1.2% q-o-q this quarter. Landlords are still flexible and favour tenant retention over occupancy.

CBRE believes that recovery of the retail sector will be highly dependent on the global vaccine roll-out and how soon Singapore can reopen. That said, the retail sector is still challenged by e-commerce competition and labour woes.

CBRE foresees that the investment volumes and the overall real estate market will improve with the rollout of vaccines globally, which might result in the easing of border restrictions and the return of business confidence.

Foreign interest will continue to remain strong, with funds still actively seeking out investments. Foreign investors will be looking out for investments that will give them higher returns, coupled with stability and value at the top of their minds. Grade A offices and shophouses will still be in high demand.

Find out here on why Normanton Park project sold 600 units in 1 weekend

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Subscribe to our newsletter

Top Articles

Search Articles